In the third part of our series on the Consumer Duty, we look at how servicing areas can balance efficiency and productivity drives against maintaining customer service levels.

We’ve learnt that the Financial Conduct Authority’s (FCA) Consumer Duty Policy Statement will be welcomed by consumers, but for firms this poses a number of obstacles to overcome within a strict timeframe. Firms now have under a year to understand the required changes, review existing practices, and implement controls, policies, and procedures.

The FCA are expecting firms to carry out all implementation planning by the end of October this year, is your firm ready?

1. Understanding the scope and impacts

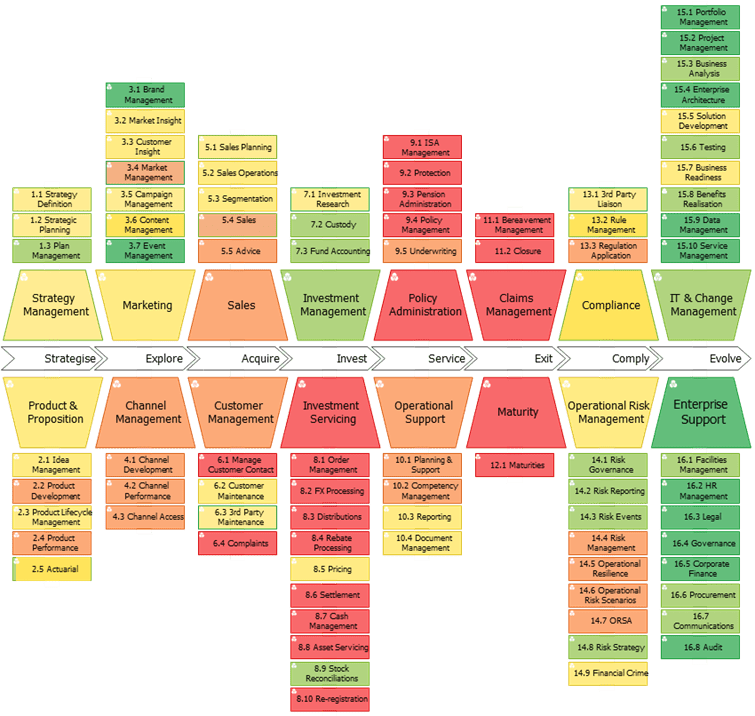

We are able to leverage SimplifyDNA to assess the impact of the Consumer Duty to all levels of a business, including their high-level capabilities and services, down to their individual processes. This can allow firms to speed up their gap analysis activities and ensure they focus on the areas which will be impacted the most.

The below image is a representative example of the gap analysis against a firm’s capabilities to highlight the areas for attention.

As part of the implementation, it’s essential to understand if existing processes are fit for purpose or are they a contributing factor to limiting customer outcomes. These will have a direct impact on service levels, which will form an important part of the Duty execution, ensuring balance for end-to-end customer journeys.

2. Process Efficiency v Customer Outcomes

“Customer service levels do not always enable consumers to get the full benefit from their products and services and this is typically caused by servicing processes that are deliberately designed to create barriers …” Ref: FCA Publications CP21/13: A new Consumer Duty.

The FCA wants to ensure firms provide a level of customer service that meets the needs of consumers throughout the tenure of the relationship. This means ensuring that service levels don’t degrade over time, particularly when a product or service moves to off-sale. It’s unacceptable for firms to give consistently poor or excessively slow service; it will be the responsibility of the firm to address these issues and embed changes in readiness for July 23. The challenge set out to senior leaders is to balance process efficiencies, in-line with strategic objectives whilst maintaining favourable customer outcomes.

Other concerns raised by the FCA, which won’t be acceptable include:

- Channels of support that do not meet the needs of customers

- Under-resourced customer helplines

- Phone systems, menus or webchats that are difficult to navigate

- Badly designed websites that make it difficult for customers to find key information online

- Uncertainty around how or where to access support

- Poor hand-off processes, including where third parties are involved

3. Metrics

Firms need to understand the metrics they are going to be governed on and put in the correct controls and processes for accurate data monitoring and recording to meet these. They will be relevant to your business and processes – firms that are online only are likely to have a greater focus on online journey’s, website response times and ease of access for consumers over those that operate on a face-to-face basis or have large contact centres.

A look at traditional call centres and call waiting times, average handling times and abandonment rates have long been a bugbear of leaders and customers alike. Balancing the need to satisfy customer needs year-round, managing busy periods such as tax year end and dealing with staff attrition and absence means it’s already extremely difficult to get right.

Do you think these changes will impact current call volumes and handling times – will this drive a change in the number of Complaints raised?

4. A Duty to those more vulnerable

The FCA has referenced additional changes for vulnerable customers as part of Customer Duty, as firms still need to do more to identify, protect and better meet their needs. The Duty raises the standard of care afforded to vulnerable customers, ensuring outcomes are as good as those for other consumers.

The guidance for firms is as follows:

- Holding focus groups with customers with characteristics of vulnerability or consumer representatives at the development stage to get a greater understanding of their needs and how products can meet them

- Exploring resources provided from, and consulting with, specialist organisations offering information on how the needs of customers with characteristics of vulnerability can be met in the design stage

- consulting with customers or representative groups when seeking to alter or withdraw a product

- Employing third-sector organisations who can review products from the viewpoint of customers with characteristics of vulnerability

Firms will need to demonstrate that its products and services are fair value for different groups of consumers, including those in vulnerable circumstances or with protected characteristics.

5. Servicing considerations

Despite a number of attempts by the FCA to improve outcomes for customers, they remain frustrated with the number of failings within firms. To ensure alignment to the core principles, it will be important for firms to:

- Review, assess and resolve quality issues across consumer channels such as telephony, post, and e-mail and ensure consistent levels of service are provided throughout.

- Review all business processes and ensure a customer focuses approach is evident throughout.

- Be clear on outsourcing responsibilities. Where firms are outsourcing or using a third-party provider, the usual regulatory principle applies in that firms are responsible and accountable for all the regulatory responsibilities applying to outsourcing and third-party arrangements.

- Ensure continuous monitoring of services to ensure that they remain consistent with the identified need for the target market and deliver the expected outcomes.

- Ensure robust data monitoring process are in place across servicing channels to identify:

At Simplify, we can help with all aspects of optimisation; from analysing processes, improving customer journeys to delivering digital and regulatory change and so much more. If you would like to harness the power of SimplifyDNA to support your firm, get in touch with us today.

..

Chris Lamb

Wealth Consultant