You can build or lose real customer trust in a single transaction. I recently changed my name after getting married. A life update that comes with joy, celebration and inevitably paperwork. In a world of biometrics, instant payments and AI everything, I assumed the process would be seamless. Maybe even invisible. After all, how complicated could something as routine as a name change possibly be?

Spoiler: very.

What followed, at least for one international credit provider, could have been a sketch straight out of Yes, Prime Minister:

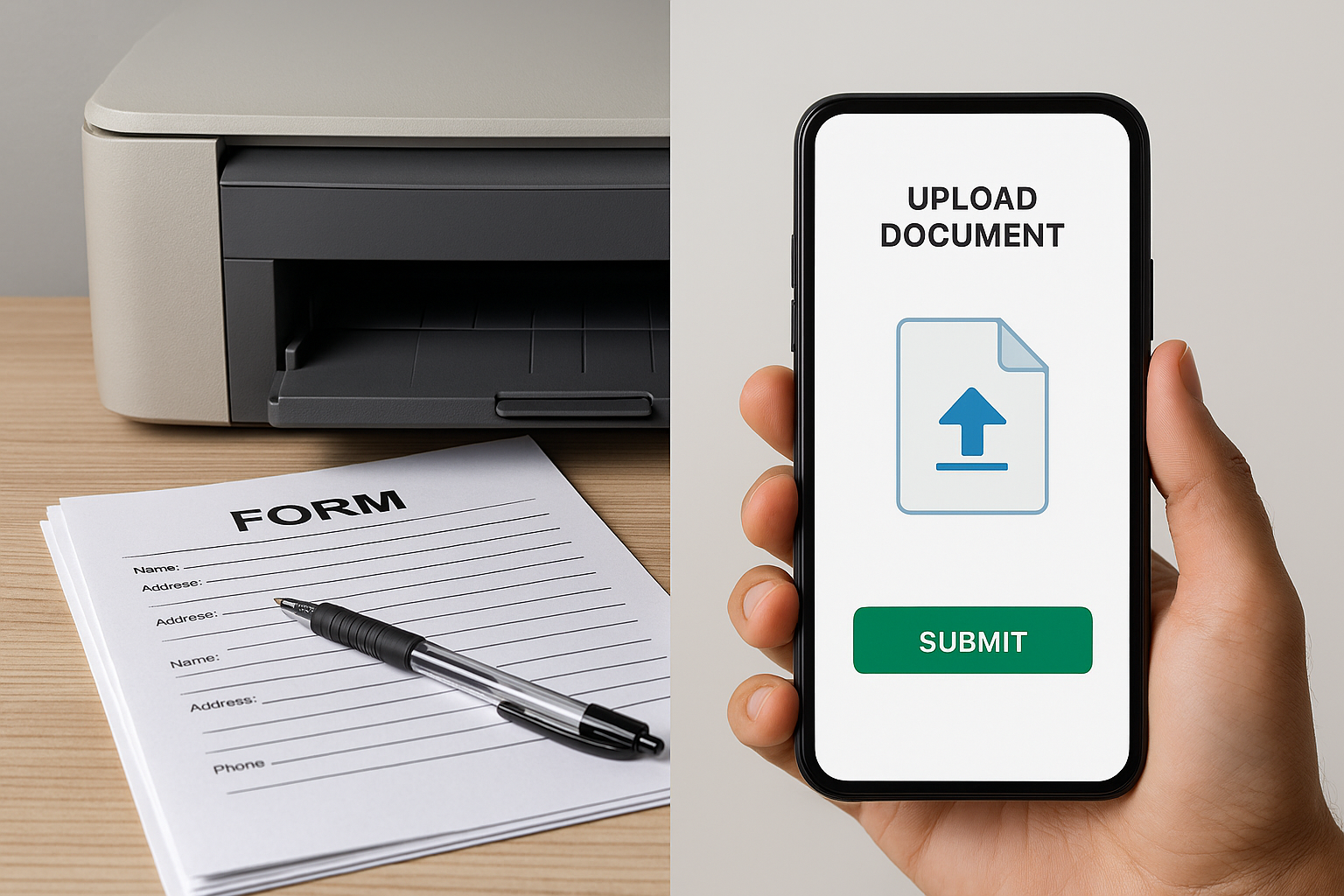

- Hunt for “Change Details.”

- Realise I need a printer, rescue it from the loft, discover the ink’s now a fossil.

- Order ink.

- Print the form (so digital!).

- Fill it out in black ink and block capitals (of course).

- Snap a photo.

- Send via online message.

The process worked and that’s the important part. But it raised an unavoidable question: if we’ve already invested in digital channels, authentication and messaging, why are we still passing handwritten paper through them?

The technology was modern. The process was not.

Next, I updated my name with a smaller so‑called “disruptor” bank. No paper. No printing. No ink cartridges crying in the corner slowly drying up.

Instead, the entire journey happened inside a smartphone app:

Log in. Select “Personal details.” Upload documentation. Submit. Confirmation received. Job done.

Two organisations, both in the financial space. Two very different experiences.

The contrast wasn’t about budget or scale. One was a large and long-established organisation. The other was smaller, newer and built with digital experiences at its core. The difference is simple. One organisation streamlined the journey, the other digitised the paperwork.

“Merely sending paper forms through a digital channel does not create a true digital journey.”

The name-change process is statistically an edge case, about 60,000 a year, compared with millions of daily transactions and around 500,000 bereavements annually. Notably, the average age for a name change in the UK is about 36, right at the peak of financial activity in adulthood. With that in mind it’s precisely these edge cases that build real customer trust.

With the current technology available, organisations have the tools to truly modernise even the most complex processes. It is possible to deliver seamless, secure customer journeys that move beyond simply digitising old paperwork. By leveraging AI, orchestration layers and process optimisation, we can minimise manual effort, reduce errors and create experiences that reflect how people live and interact today. Rather than accepting clunky workarounds as inevitable. it’s time to embrace solutions that make every interaction, no matter how infrequent, feel effortless and digital from start to finish.

Both of my name changes were successful in the end. Marriage still going strong (helpful, given this whole blog would be awkward otherwise). The disruptor bank left me quietly impressed. And the printer? Smugly back in storage, waiting for its next cameo in the so‑called “digital age.”

But the point stands:

Digital transformation isn’t about adding digital steps to analogue workflows. It’s about rethinking the journey end‑to‑end. Even the ones that don’t happen every day.

Richard Unaka

Technology Consultant